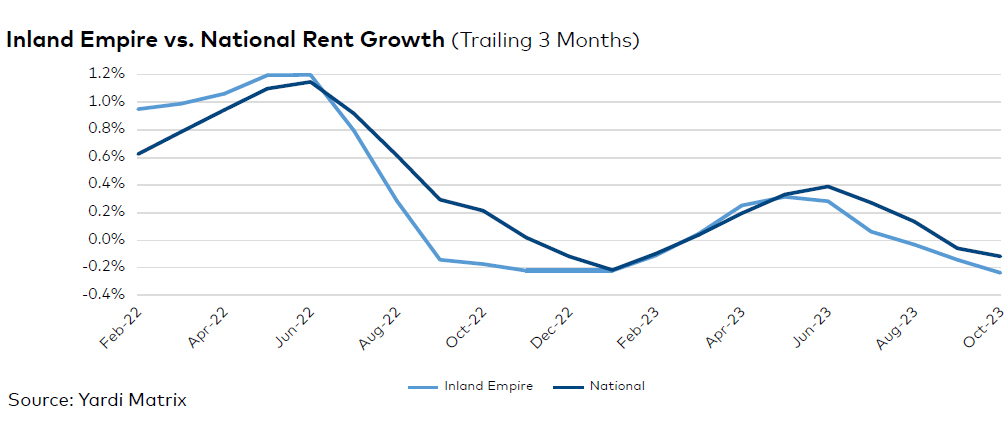

The Inland Empire’s multifamily market entered the fourth quarter of 2023 during a challenging period, with rent movement turning negative, employment growth softening considerably and investment and supply still down. Yet rates decreased just 0.2 percent on a trailing three-month basis, to $2,113, while the U.S. figure slid 0.1 percent, to $1,718 through October. The metro’s occupancy fell 110 basis points in the 12 months ending in September, to 95.3 percent.

Inland Empire unemployment stood at 4.9 percent in September, according to data from the Bureau of Labor Statistics. The rate was 50 basis points higher than the January figure, trailing the U.S. (3.8 percent) and right behind California (4.7 percent). Meanwhile, in the 12 months ending in August, the area added 24,400 positions for a 0.8 percent expansion, heavily lagging the 2.5 percent national average. Additionally, four sectors lost 8,500 jobs combined, with trade, transportation and utilities, a local staple, accounting for roughly two-thirds of that. Job growth was primarily sustained by the education and health services (12,800 jobs) and government (7,500 jobs) sectors.

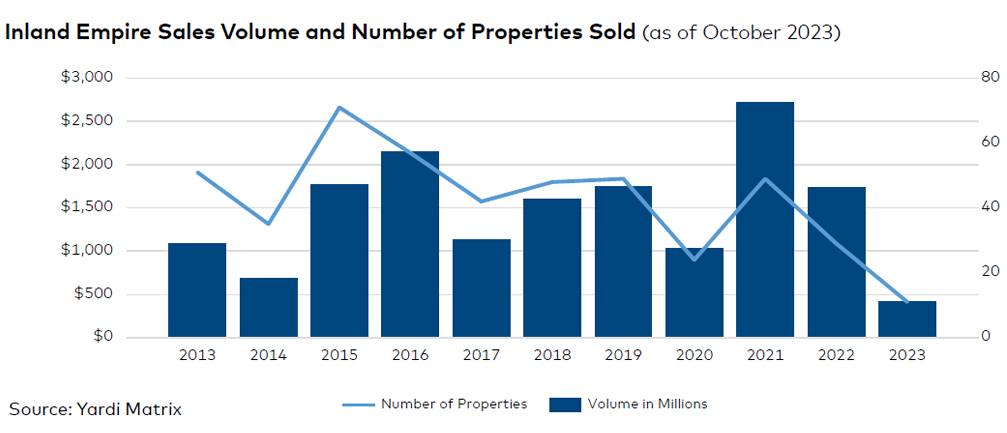

Development softened, with 571 units delivered in 2023 through October and an additional 6,963 units under construction. The volume of new projects decreased by 7.1 percent year-over-year but remained steady. Investment activity amounted to just $414 million during the year’s first 10 months, for a price per unit that declined 14.5 percent year-to-date, to $260,953 as of October.

Read the full Yardi Matrix report.