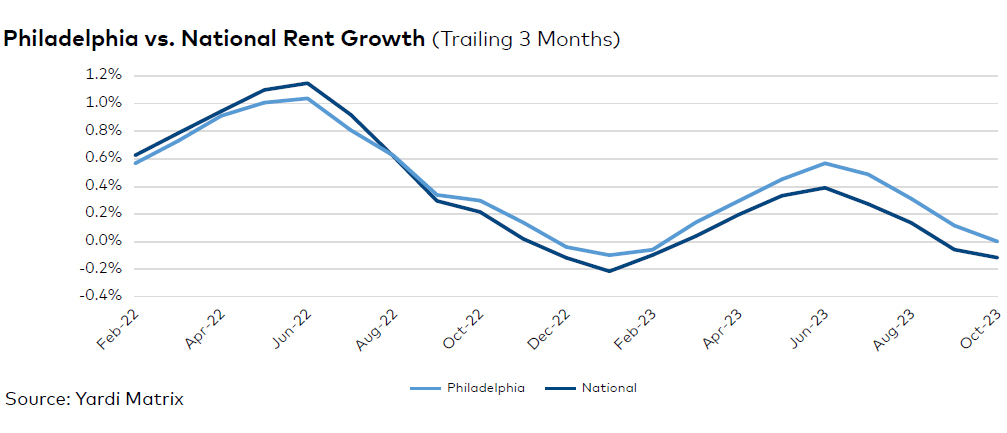

Philadelphia’s multifamily market displayed healthy fundamentals entering the fourth quarter. Amid slowing absorption, rents were still up 2.1 percent on a year-over-year basis, reaching $1,728, while the national figure advanced just 0.4 percent, to $1,718 as of October. On a trailing three-month basis, Philadelphia rates were flat, while the U.S. average dropped 10 basis points. Meanwhile, the occupancy rate in stabilized assets dropped just 30 basis points in 12 months, to a relatively tight 96.0 percent as of September.

Philadelphia’s employment market added 98,100 new jobs in the 12 months ending in August, for a 3.0 percent expansion. Although all sectors added jobs, just two sectors–education and health services (38,500 jobs) and leisure and hospitality (20,000 jobs)–accounted for more than half of the positions added. The metro’s unemployment rate stood at a tight 3.5 percent as of September, according to the Bureau of Labor Statistics, virtually on par with Pennsylvania (3.4 percent) and surpassing the national average (3.8 percent).

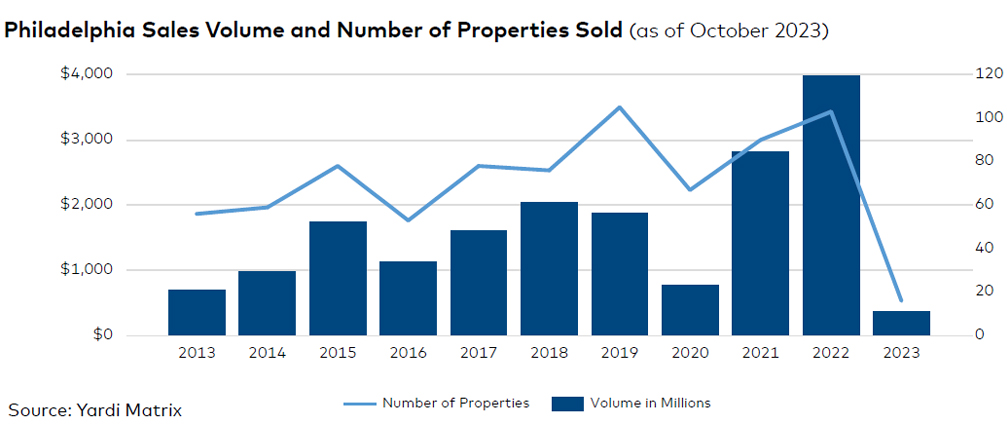

A total of 3,408 units came online in the first 10 months of 2023, with an additional 18,794 units under way as of October. Meanwhile, only $368 million in multifamily assets traded in 2023 through October, a fraction of 2021 and 2022’s record numbers, as national and global economic trends caught up with the rental market.

Read the full Yardi Matrix report.